529 Plans 101

Comparing 529 Plans, UTMA Accounts, and Roth IRAs: Which is the Best Option for Education Savings?

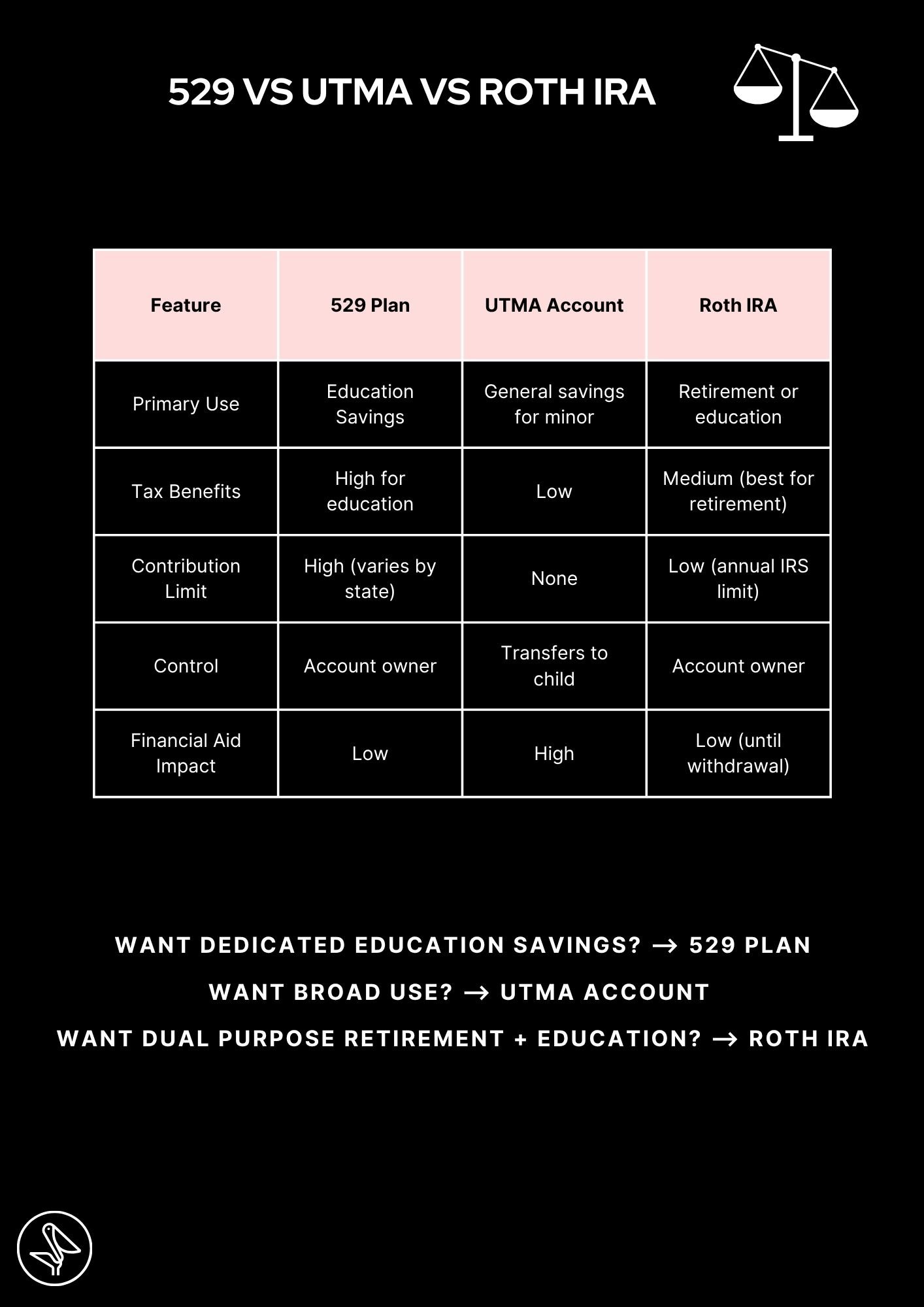

Navigating the landscape of education savings can be overwhelming, with various options available to families. Among these, 529 savings plans, UTMA accounts, and Roth IRAs stand out as popular choices. Each comes with its own set of advantages and considerations, making it crucial for families to understand how these options stack up against each other. In this comprehensive guide, we’ll compare 529 plans, UTMA accounts, and Roth IRAs in terms of taxes, use of funds, and impact on financial aid, helping you make an informed decision about the best option for your education savings goals.

The 3 most important considerations are:

Taxes

Use of funds

Financial aid

529 College Savings Plans

529 plans were created to help families save for the rising costs of education, particularly higher education. These plans are named after Section 529 of the Internal Revenue Code, which established them.

A 529 savings plan is tailored specifically for education savings and offers unique tax advantages, making it a popular choice.

Tax-Free Growth: While the contributions are made with after-tax dollars, the investment grows tax-free, and withdrawals for qualified education expenses are also tax-free at the federal level.

State Tax Deductions: Most states offer additional tax incentives, such as tax deductions or credits, to encourage residents to save in their state’s plan.

Use of Funds: Funds from 529 plans can be used for a variety of qualified education expenses, not just tuition. This includes expenses like books, room and board, and even K-12 tuition in some cases. Non-educational withdrawals may incur taxes and penalties.

Financial Aid- For example, 529 plans are considered a parental asset and are factored into the Expected Family Contribution (EFC) calculation which determines how much parents are expected to contribute to their child’s tuition and how much they will receive in aid. However, only a portion of the 529 plan balance is counted towards the EFC (currently a maximum of 5.64% of the total balance per year).

UTMA (Uniform Transfers to Minors Act) Account:

UGMA/ UTMA accounts provide flexibility but may lack specific education-related tax benefits. are considered student assets and are factored into the EFC at a higher rate (currently 20%).

Advantages:

Provides flexibility in how funds are used, not restricted to education expenses.

No contribution limits, allowing for large contributions.

Potentially lower tax rates for children on investment gains.

Considerations:

Irrevocable Gift: Once assets are transferred to the child, they become the child’s property and can be used for any purpose once they reach a certain age (usually 18 or 21, depending on the state).

No Tax Advantages: There are no specific tax advantages for education savings.

Impact on Financial Aid: Assets held in a UTMA/ UGMA are counted at a 20% rate- a true disadvantage when compared to other plans.

Roth IRA (Individual Retirement Account):

A Roth IRA can also be a flexible option if you’re comfortable with the potential limits on contributions and earnings. They are not factored at all into the EFC but will be considered untaxed income when withdrawn that will be factored into the following year’s FAFSA application.

Advantages:

Can be used for education expenses without penalties.

Flexibility: Funds can also be used for retirement if not needed for education.

Tax-Free Withdrawals: Contributions (not earnings) can be withdrawn at any time without taxes or penalties when used on qualified education expenses.

Considerations:

Contribution Limits: Contributions are subject to annual limits.

Earnings Restrictions: Earnings may be subject to taxes and penalties if not used for qualified education expenses.

529 plans and Roth IRA accounts can now work in tandem. In December 2022, a significant legislation was passed by Congress, introducing a new provision that allows tax- and penalty-free rollovers from 529 plans to Roth IRA accounts starting in 2024. This development provides families with increased flexibility in their financial planning for future educational expenses as families can transfer any unused or excess funds from a college savings account into a Roth IRA without facing unfair penalties.

To qualify for this rollover, the Sec. 529 account must have been in existence for more than 15 years at the time of the rollover, and the aggregate rollovers cannot exceed $35,000. Additionally, the rollovers are subject to the annual contribution limits of Roth IRAs.

The best choice depends on your financial goals and individual circumstances.

The most important thing is to have a plan and make sure that works for you.